Business Licenses in Singapore: A 2026 Guide

Discover essential information on business licenses in Singapore. Ensure compliance and protect your investment with our 2026 guide. Read more!

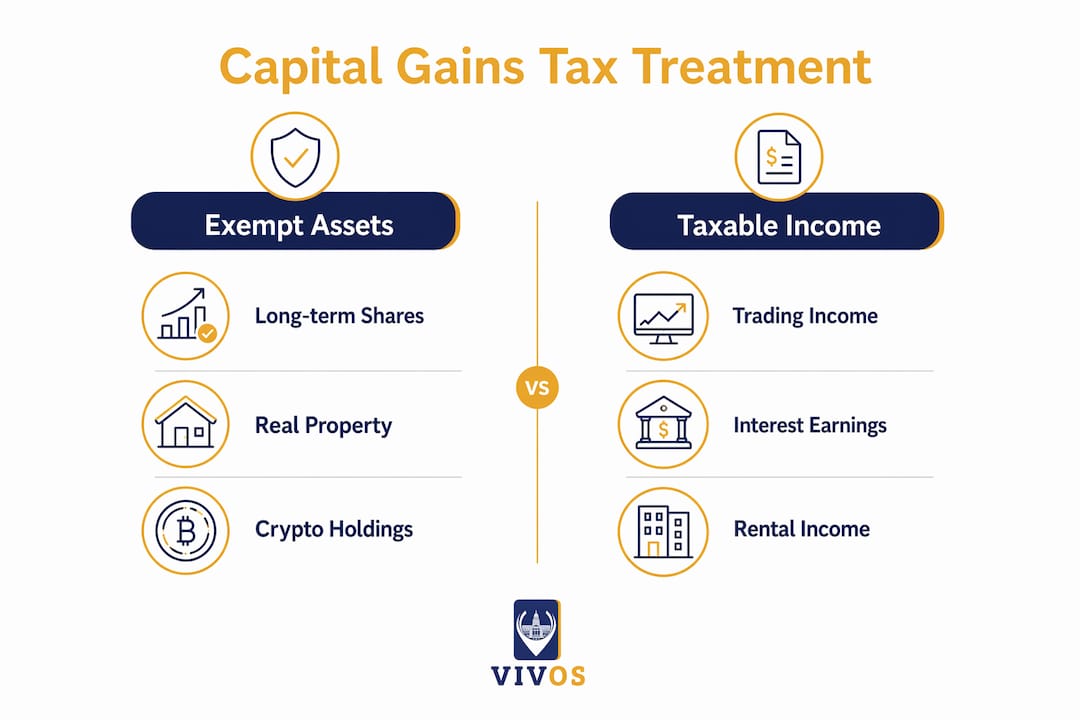

Singapore is defined as one of the few developed economies with no capital gains tax on profits from selling shares, property, bonds, or crypto assets held as long-term investments. The Inland Revenue Authority of Singapore (IRAS) governs this under the Income Tax Act 1947, section 10(1), which taxes trading income but leaves genuine capital gains untouched. That distinction matters enormously. If IRAS determines your investment activity resembles trading, your gains become taxable at personal income tax rates up to 24% for residents earning over SGD 1,000,000. Understanding capital gains tax Singapore rules is not optional for serious investors. It is the foundation of sound tax planning here.

Singapore levies no capital gains tax on assets held genuinely for long-term investment purposes. That covers shares, real property, bonds, and crypto assets. The exemption is not automatic, though. It depends entirely on the nature of your activity.

Singapore law draws a clear line between capital gains and trading income. Capital gains arise when you sell an asset you held as an investment. Trading income arises when buying and selling assets is your business or primary profit-seeking activity. IRAS taxes trading income under Income Tax Act section 10(1). Capital gains face no tax at all.

| Scenario | Classification | Tax Treatment |

|---|---|---|

| Selling shares held for 5 years with no active trading | Capital gain | Exempt from tax |

| Buying and selling shares weekly for profit | Trading income | Taxable at personal rates |

| Selling a rental property after 10 years | Capital gain | Exempt from tax |

| Flipping multiple properties within 12 months | Trading income | Taxable at personal rates |

| Holding Bitcoin for 3 years, then selling | Capital gain | Exempt from tax |

| Running a crypto trading desk | Trading income | Taxable at personal rates |

The intent behind your purchase is the deciding factor. IRAS looks at what you planned to do with the asset when you bought it, not just what you did with it later.

Pro Tip: Write a brief investment rationale memo when you buy any significant asset. Date it, sign it, and store it with your purchase records. This contemporaneous document is your first line of defense in any IRAS inquiry.

IRAS applies the “badges of trade” test to decide whether gains are capital or taxable income. No single factor is decisive. IRAS weighs the combined picture of your behavior across several criteria.

The key badges of trade include:

For property investors, IRAS issues a Property Disposal Questionnaire when it suspects gains may be trading income. This questionnaire probes your purchase intent, financing, and disposal history. Receiving one is a serious signal that IRAS is scrutinizing your transaction.

Reclassification carries real cost. Trading income is taxed at up to 24% for individual residents or 17% for companies under Singapore’s corporate tax rate. That is a significant liability on gains you assumed were tax-free.

Maintaining contemporaneous records of your investment intent is the most practical protection available. Purchase rationale documents, rental agreements, and board resolutions all support a capital classification.

Pro Tip: If you face an IRAS audit or reclassification inquiry, professional tax dispute support can make a material difference in the outcome. Do not respond to IRAS questionnaires without advice.

Singapore’s no-capital-gains-tax rule applies broadly, but each asset class carries its own nuances. The table below summarizes the key positions.

| Asset Class | Capital Gain Treatment | Other Tax Considerations |

|---|---|---|

| Shares | Exempt if held long-term | Dividends are tax-exempt under the one-tier system |

| Real property | Exempt if held long-term | Buyer’s Stamp Duty, Additional Buyer’s Stamp Duty apply |

| Crypto assets | Exempt if held long-term | Taxable if IRAS classifies activity as a trading business |

| Bonds and securities | Exempt if held long-term | Interest income may be taxable depending on source |

| Business assets | Generally exempt | Depreciation recapture rules may apply |

Long-term share investors pay no tax on capital gains. Singapore-sourced dividends are tax-exempt under the one-tier corporate tax system, which eliminates double taxation at the shareholder level. High-frequency traders who buy and sell shares as a business activity face a different outcome. IRAS can classify their profits as trading income subject to personal income tax.

Property gains are exempt from capital gains tax when the property is held long-term as an investment. However, stamp duties apply to every property purchase regardless of holding period. The Additional Buyer’s Stamp Duty (ABSD) can reach up to 60% for foreign purchasers. Rental income from property is fully taxable at marginal personal income tax rates. These are separate obligations that exist alongside the capital gains exemption.

IRAS treats crypto assets as digital payment tokens. Long-term holdings are exempt from tax. Active crypto trading, where buying and selling tokens is your primary business, is taxable as trading income. IRAS published guidance on this distinction in 2020, and the framework remains the operative standard in 2026.

Bond gains are generally exempt as capital gains. Interest income may be taxable depending on its source and your tax residency status. Foreign-sourced income remitted to Singapore is generally not taxable for individuals unless it constitutes trading income.

Capital gains are not reported as taxable income unless IRAS reclassifies them. You do not file a capital gains schedule. You do not calculate a capital gains figure for your tax return. The exemption is structural, not elective.

What you do report are income streams that arise alongside your investments:

For detailed guidance on filing personal income tax in Singapore, including income from rental and investment sources, Vivos provides structured support for both residents and non-residents. Annual tax filing procedures and deadlines are covered in full for individuals managing multiple income streams.

Understanding pass-through taxation structures is also relevant for investors who hold assets through partnerships or trusts, where income attribution rules affect how gains and income are reported.

Singapore’s capital gains exemption is real and broad, but it is conditional on investor behavior, documentation, and asset holding patterns that IRAS actively scrutinizes.

| Point | Details |

|---|---|

| No capital gains tax in Singapore | Gains from shares, property, bonds, and crypto are exempt if held as long-term investments. |

| Reclassification risk is real | IRAS can tax gains as trading income at rates up to 24% if your behavior resembles a trading business. |

| Badges of trade determine classification | Frequency, holding period, profit motive, and financing method all factor into IRAS’s assessment. |

| Rental income is always taxable | Property capital gains are exempt, but rental income is taxed at marginal rates for residents and 24% for non-residents. |

| Documentation is your best protection | Contemporaneous records of investment intent are the primary defense against reclassification audits. |

Most investors I work with focus on the headline: no capital gains tax. They stop there. That is the wrong place to stop.

The real risk in Singapore is not the tax rate. It is the reclassification. IRAS does not need to prove you intended to trade. It needs to show that your behavior, taken as a whole, looks like trading. Frequency, short holding periods, and large transaction volumes are enough to trigger a questionnaire. Once that questionnaire arrives, you are already in a defensive position.

What I have seen work consistently is simple: write down why you bought the asset before you buy it. Not after. Not when IRAS asks. Before. A dated memo stating your investment rationale, expected holding period, and income strategy takes ten minutes to write. It can save tens of thousands of dollars in reclassification tax and professional fees.

The Singapore tax system’s simplicity is a genuine advantage for investors. The one-tier corporate tax system, the absence of capital gains tax, and the exemption on foreign-sourced income for individuals all reduce friction. But simplicity at the policy level does not mean simplicity at the individual level. The badges of trade test is fact-intensive. Every transaction adds to the pattern IRAS sees.

My advice: hold longer, trade less, document everything, and get professional advice before you sell a significant asset. The cost of advice is always lower than the cost of a reclassification audit.

— Ray

Navigating Singapore’s tax rules on investment income, rental returns, and potential trading income reclassification requires precise, current expertise.

Vivos provides corporate secretarial services and tax compliance support for individual investors and businesses operating in Singapore. The Vivos team handles personal income tax filing, annual tax submissions, and IRAS audit support for clients managing property, shares, crypto, and other investment assets. Whether you need to structure your holdings correctly from the start or respond to an IRAS inquiry, Vivos delivers clear, compliant solutions. Contact Vivos to arrange a consultation on your Singapore tax obligations.

Singapore does not levy capital gains tax on profits from selling shares, property, bonds, or crypto assets held as long-term investments. Gains are only taxable if IRAS reclassifies them as trading income under Income Tax Act section 10(1).

The badges of trade test is the framework IRAS uses to determine whether gains are capital or taxable trading income. It evaluates frequency of transactions, holding period, profit-seeking motive, financing method, and the nature of the asset.

Yes. Rental income is taxable at progressive personal income tax rates for residents and at a flat 24% for non-residents, even though capital gains on property sales are exempt.

IRAS classifies crypto assets as digital payment tokens. Long-term holdings are exempt from tax. Active trading in crypto is treated as a business activity and taxed as trading income.

Reclassified gains are treated as trading income and taxed at personal income tax rates up to 24% for residents or at the 17% corporate tax rate for companies. Maintaining clear documentation of investment intent is the primary way to defend against reclassification.

2 January, 2025

2 January, 2025 2 January, 2025

2 January, 2025

Discover essential information on business licenses in Singapore. Ensure compliance and protect your investment with our 2026 guide. Read more!

Discover key insights on unaudited financial statements in Singapore. Learn the requirements, exemptions, and responsibilities for business owners.

Discover the key steps for successful annual return filing in Singapore. Avoid penalties and ensure compliance with our 2026 guide.