Annual Return Filing in Singapore: 2026 Guide

Discover the key steps for successful annual return filing in Singapore. Avoid penalties and ensure compliance with our 2026 guide.

Unaudited financial statements are financial documents prepared in accordance with Singapore Financial Reporting Standards (SFRS) without undergoing an external audit, serving as official statutory reports for eligible companies. For business owners in Singapore, these reports are not optional summaries or internal spreadsheets. They are legally required documents that satisfy obligations with the Accounting and Corporate Regulatory Authority (ACRA) and the Inland Revenue Authority of Singapore (IRAS). Understanding unaudited financial statements in Singapore means knowing exactly who qualifies, what must be included, and what directors are personally responsible for signing.

Audit exemption is a legal status, not a blanket permission to skip financial reporting. Audit exemption does not mean reporting exemption. Every company must still prepare full statutory financial statements annually under SFRS, regardless of whether an external auditor reviews them.

To qualify as a small company exempt from statutory audit, your company must meet at least two of these three criteria for two consecutive financial years:

This two-of-three threshold applies across two consecutive years, not just the most recent one. A company that briefly dips below the thresholds in a single year does not automatically qualify. Consistency across two years is the standard.

Small group exemptions follow a parallel structure. If your company is part of a group, the group as a whole must also qualify as a small group under the same criteria applied at the consolidated level. A subsidiary that individually qualifies may still require an audit if its parent group does not meet the thresholds.

One common misconception is that audit exemption reduces compliance obligations. It does not. The financial statements must still present a true and fair view of the company’s financial position, comply with SFRS, and be filed with ACRA on time.

Pro Tip: If your company is approaching the S$10 million revenue threshold, track your figures across both financial years carefully. Crossing even one threshold in both years can trigger a mandatory audit requirement.

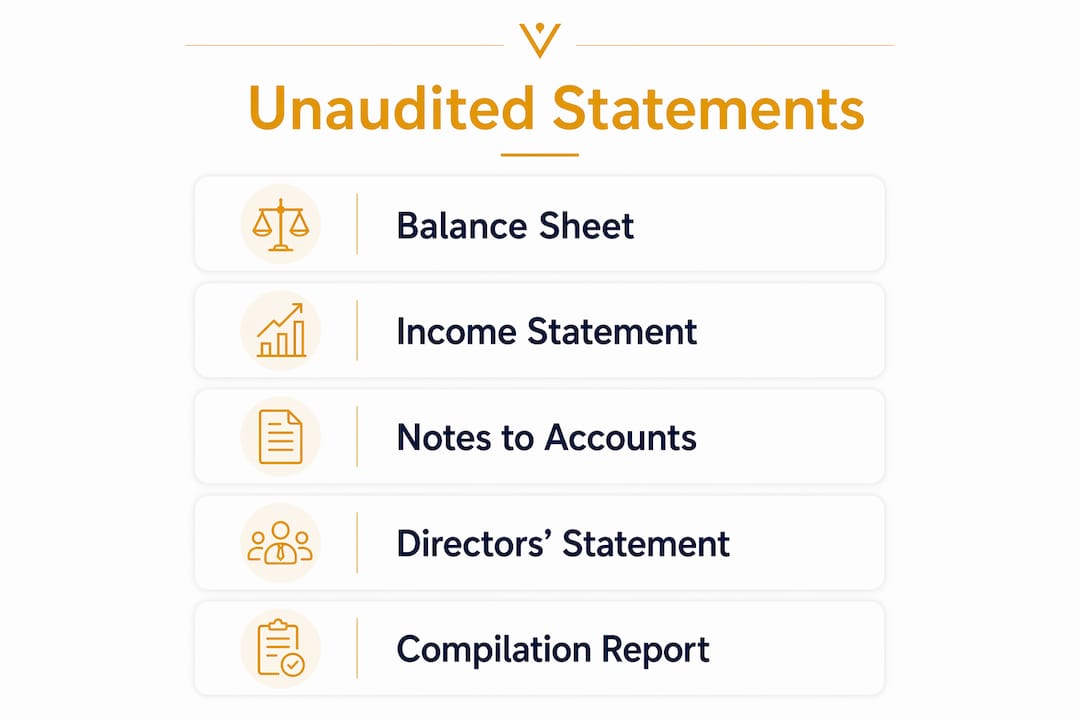

The required components of unaudited financial statements under SFRS are the same as those for audited statements, minus the auditor’s report. SFRS-compliant statements must include the following:

The Notes to the Accounts deserve particular attention. Mandatory disclosure notes must cover accounting policies, key judgments, and future obligations such as leases and legal contingencies. Without complete notes, the financial statements are non-compliant, regardless of how accurate the numbers appear.

The table below summarizes each component and its primary compliance function:

| Component | Primary Compliance Function |

|---|---|

| Balance Sheet | Confirms financial position at year-end for ACRA filing |

| Profit & Loss Statement | Supports IRAS tax computation and ECI filing |

| Cash Flow Statement | Demonstrates liquidity for banks and grant agencies |

| Statement of Changes in Equity | Tracks retained earnings and capital movements |

| Notes to Financial Statements | Discloses policies and risks; required for SFRS compliance |

A professional compilation report from a qualified accountant adds a layer of credibility to these statements. The accountant does not audit the figures but compiles them into a format that meets SFRS standards and withstands scrutiny from ACRA, IRAS, and financial institutions.

Directors carry direct legal responsibility for the accuracy of financial statements, audited or not. The Directors’ Statement is a mandatory declaration that must accompany every set of financial statements filed with ACRA. At least two directors must sign the Directors’ Statement, confirming that the reports give a true and fair view of the company’s financial affairs.

This signature is not a formality. Signing the Directors’ Statement carries personal legal liability under the Singapore Companies Act. If the statements are inaccurate or misleading, directors can face regulatory action, fines, or personal financial exposure. This applies equally to unaudited statements.

Directors should treat financial statements as governance records, not mere compliance paperwork. The signed statement legally affirms the company’s financial health and protects directors from regulatory risk when prepared correctly.

Specific situations require additional steps:

Understanding director duties and liabilities in Singapore go beyond signing documents. Directors must actively review the financial statements before signing, not simply rely on the preparer’s assurances.

Pro Tip: Never sign a Directors’ Statement without reviewing the underlying figures. If you do not understand a line item, ask your accountant to explain it before you sign. Personal liability attaches the moment your signature appears on the document.

Unaudited financial statements do more than satisfy ACRA filing requirements. They serve as working tools for tax planning, cash flow management, and business financing. SMEs use these reports to meet IRAS requirements, secure bank loans, and make informed operational decisions at a fraction of the cost of a full audit.

The cost advantage is real. A full statutory audit costs significantly more than a professional compilation engagement. For companies that qualify for audit exemption, unaudited statements deliver the same compliance outcome and stakeholder credibility at lower cost.

Pro Tip: Use your Cash Flow Statement as a monthly management tool, not just an annual filing document. Tracking cash inflows and outflows monthly gives you early warning of liquidity problems and strengthens your position when approaching banks for a corporate banking solution.

Unaudited financial statements in Singapore are legally required, SFRS-compliant reports that every audit-exempt company must prepare annually, covering tax, compliance, and financing needs.

| Point | Details |

|---|---|

| Audit exemption is not reporting exemption | All companies must prepare full SFRS-compliant statements annually, regardless of audit status. |

| Small company criteria are specific | Meet at least two of three thresholds (revenue, assets, employees) across two consecutive years. |

| Directors carry personal liability | The Directors’ Statement requires at least two signatures and exposes signatories to legal risk if inaccurate. |

| All five components are mandatory | Balance Sheet, P&L, Cash Flow, Changes in Equity, and Notes must all be included under SFRS. |

| Professional compilation adds credibility | Compiled statements meet ACRA and IRAS standards and satisfy banks and investors without a full audit. |

The most common mistake I see among Singapore entrepreneurs is treating audit exemption as a green light to deprioritize financial reporting. Business owners hear “you don’t need an audit” and assume their obligations are minimal. That assumption creates real risk.

The distinction between unaudited and unprofessional financial statements is critical. Internal spreadsheets, simplified summaries, or bookkeeping exports do not meet statutory standards. ACRA expects full SFRS-compliant statements, complete with Notes to the Accounts, every year without exception.

Directors also underestimate what they are signing. The Directors’ Statement is a legal declaration, not a cover page. Signing it without reviewing the underlying figures is the kind of shortcut that creates personal liability exposure. Regulations in Singapore are not static, and ACRA has consistently tightened enforcement around financial disclosure standards.

The businesses that handle this well treat their unaudited statements as a governance tool. They review the figures quarterly, use the Cash Flow Statement to manage liquidity, and engage professional compilers who understand SFRS. That approach costs less than an audit and delivers far more value than a last-minute filing.

— Ray

Preparing SFRS-compliant financial statements requires more than good bookkeeping. It requires structured compilation, accurate disclosure notes, and a clear understanding of ACRA and IRAS requirements.

Vivos provides financial accounting and reporting services tailored for Singapore SMEs and startups, covering the full preparation of unaudited financial statements, Directors’ Statements, and compilation reports. The Vivos team reduces director workload, minimizes compliance risk, and produces statements that satisfy ACRA filings, IRAS tax submissions, and bank financing requirements. For business owners who want accurate, defensible financial records without the cost of a full audit, Vivos offers corporate secretarial services that cover the entire reporting cycle from compilation to filing.

Unaudited financial statements are SFRS-compliant statutory reports prepared without an external auditor’s review. They are legally required for all Singapore companies, including those exempt from audit under the small company criteria.

A company qualifies as a small company if it meets at least two of three criteria for two consecutive years: annual revenue of S$10 million or less, total assets of S$10 million or less, and 50 or fewer employees.

A compilation report is a document prepared by a professional accountant who organizes a company’s financial data into SFRS-compliant statements without auditing the figures. It adds credibility and ensures the statements meet regulatory standards.

The Directors’ Statement is a mandatory legal declaration confirming that the financial statements give a true and fair view of the company’s affairs. At least two directors must sign it, unless ACRA grants relief for single-director companies.

Yes. Banks and financial institutions in Singapore accept professionally compiled unaudited financial statements when assessing loan applications, provided the statements are SFRS-compliant and prepared by a qualified accountant.

2 January, 2025

2 January, 2025 2 January, 2025

2 January, 2025

Discover the key steps for successful annual return filing in Singapore. Avoid penalties and ensure compliance with our 2026 guide.

Yes — a non-resident founder can open a Singapore business bank account without living in Singapore, and in most cases without flying in. Fintech accounts…

Short answer: it depends on where your customers are, who your investors are, and what happens when you pay yourself. Delaware wins for US-only ventures,…